Is Your Renewal Strategy Just Shifting Costs to Employees?

It doesn’t have to be that way. At Fox Everett, we help you break the cycle of cost-shifting and start creating lasting solutions. Our self-funded GAP plans allow you to raise deductibles strategically, then reinvest the savings into tailored coverage that lessens the burden on your team. You can keep your renewal increases under control while improving benefits and increasing retention. We take care of the data, design, and administration, so you can focus on results, not uncertainty.

$150M+

in Annual Claims

80+

Years of Expertise

24,000+

Members

Why Self-Funding with GAP Builds Long-Term Savings

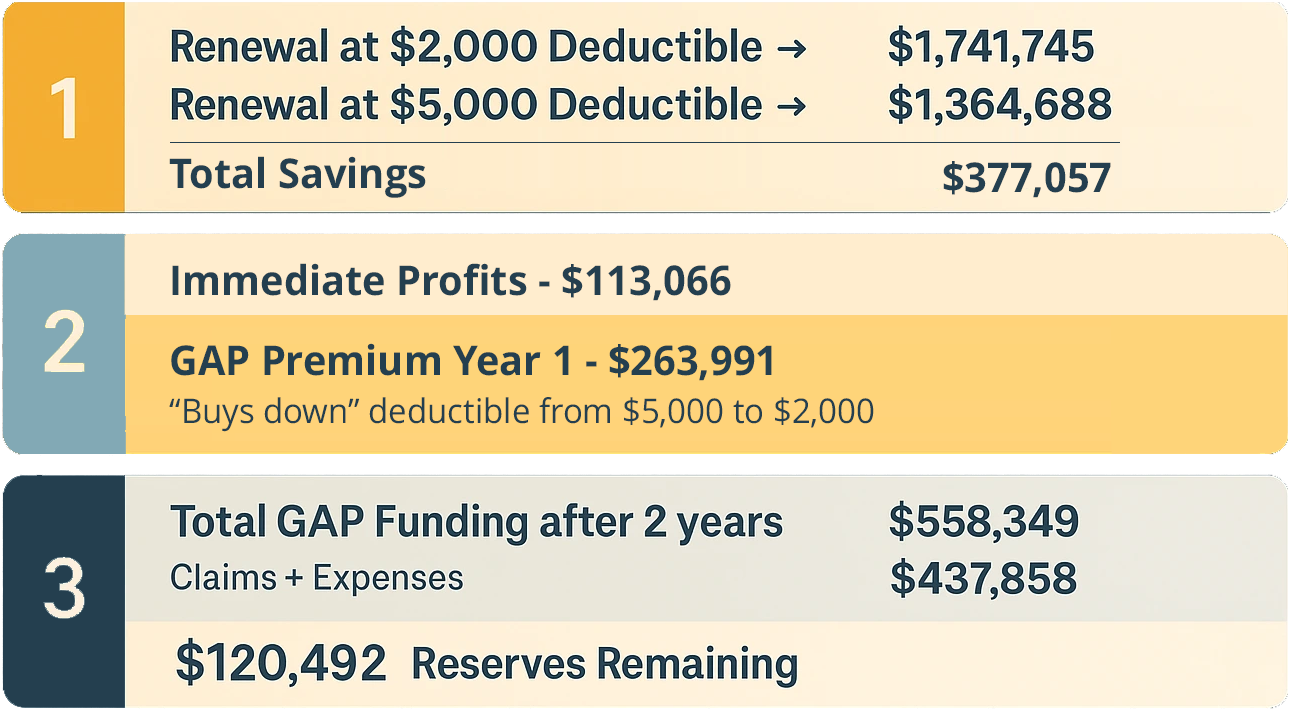

A self funded plan keeps more of your dollars working for you. By raising the deductible, you lower premiums and create measurable savings. Fox Everett helps you use part of those savings to fund a GAP plan that buys the deductible back down for employees, keeping their experience the same. Any remaining savings stay with the employer as reserves, growing each year to offset renewals and strengthen long term financial stability. The result is sustainable cost control, richer benefits, and lasting savings that keep your dollars in your business.

How a Self-Funded GAP works

GAP claims are only triggered AFTER the “buy down” deductible is met.

1. Present ID Card

Member shows ID cardat time of service.

2. Verify Benefits

Provider confirms eligibility with Fox Everett.

3. Provide Service to Member

Provider files claim directly with Fox Everett .

4. File Claim to Carrier

Medical Carrier processes claim and sends the Explanation of Benefits (EOB) to the member and provider.

5. Submit to Fox Everett

Provider sends the EOP and claim to Fox Everett.

6. Pay Provider

Fox Everett processes the claim and sends payment to the provider.

Who is a good fit for a

Self-Funded GAP Plan?

Fully insured groups facing rising renewal costs can benefit from self-funded GAP strategies. Ideal for employers with 50+ enrolled or existing GAP plans, this approach offers cost control, stability, and protection from high out-of-pocket expenses—while keeping plan design competitive and sustainable.

Rethinking Deductibles? Let’s Talk GAP.

If rising premiums are forcing you to choose higher deductibles, a self-funded GAP plan can ease the burden on your budget and your employees. We’ll explain how to set it up, what it can save you, and why it’s a better choice than a fully insured option.

Your Questions Answered.

This FAQ provides clear answers to common questions about the Self-Funded GAP Plan, covering eligibility, coverage, claims, and benefits of enrollment. Explore the questions below to understand how it works and how it can meet your healthcare needs.

While the GAP Plan is technically a type of Health Reimbursement Arrangement (HRA), here's the key difference:

- With the GAP Plan, Fox Everett and the provider take care of managing claims and reimbursements, removing HR from the entire process.

- Fox Everett can also administer traditional HRAs if desired, but the additional claims-handling aspect of the GAP Plan makes it a more comprehensive solution for many employers.

To provide an accurate quote for your Self-Funded GAP Plan, we require:

- Renewal rates showing both the current plans as well as the rates for the Higher Deductible plans.

- Accumulator report that shows number of members who have hit their individual deductibles and OOP max.

- Number of Enrolled in each Tier (if not included on the Renewal Rates sheet)

- Any additional Claims Experience (if available)

Employers gain significant savings with a GAP Plan by:

- Raising the primary insurance deductible to reduce overall renewal premium costs.

- Reinvesting a portion of those savings into the GAP Plan, ensuring employees maintain similar out-of-pocket expenses while the employer realizes considerable cost reductions.

The claims process is seamless with Fox Everett:

- The employee shows their primary insurance card and Fox Everett GAP Plan card during the first visit to a new provider.

- The provider verifies coverage with both insurance carriers.

- Upon receiving the explanation of benefits (EOB) from the major medical plan, the provider submits the claim to Fox Everett.

- Fox Everett processes the claim and sends the payment with a corresponding EOB summary to the provider. A copy of the EOB is sent to the employee for their records.

Fox Everett stands out for its boutique-level service tailored to mid-sized employers. Here’s why businesses love working with us:

- Customizable Solutions for your specific needs.

- Hands-Free Claims Management, saving HR teams time and reducing administrative burden.

- Expertise in Mid-Market Companies, providing cost-effective and agile benefits administration.

- Flexibility to ensure continuity regardless of carrier changes.

- Superior Customer Service with dedicated reps ensuring prompt support.

Still have questions?

We’re here to help. Whether you’re looking into self-funding for the first time or need clarity on your current plan, our team is ready to give clear answers, personalized insights, and honest guidance. There’s no pressure, just partnership.