The Tipping Point:

When Self-Funding Becomes the Smart Move

Fully insured plans charge fixed premiums whether your team uses the benefits or not—meaning you often overpay. With self-funding, you only pay for what’s actually used, giving you greater control and the opportunity to keep the savings.

$150M+

in Annual Claims

80+

Years of Expertise

24,000+

Members

Which is best for your business?

If your company has over 50 employees enrolled in a health plan, it’s time to take a hard look at how you're funding it.

Most employers are familiar with the traditional fully insured model offered by big-name carriers like Blue Cross, Aetna, Cigna, and United. While fully insured premiums may feel stable and predictable each month, that consistency comes at a price, and it's often more than you're using. The truth is, no employer can outrun their own claims experience forever. You're likely paying for more than what your team consumes, with little transparency or control. Today, self-funding has gone mainstream, with strategies that put you in the driver’s seat - giving you access to your actual data, the ability to tailor your plan design, and the chance to keep unused dollars inyour business, not the carrier’s pocket.

Today, self-funding has gone mainstream, with strategies that put you in the driver’s seat - giving you access to your actual data, the ability to tailor your plan design, and the chance to keep unused dollars in your business, not the carrier’s pocket.

At a Glance

55 Employees

Baton Rouge, LA

Cost Containment Initiatves

10 Years Self-Funded

with Fox Everett

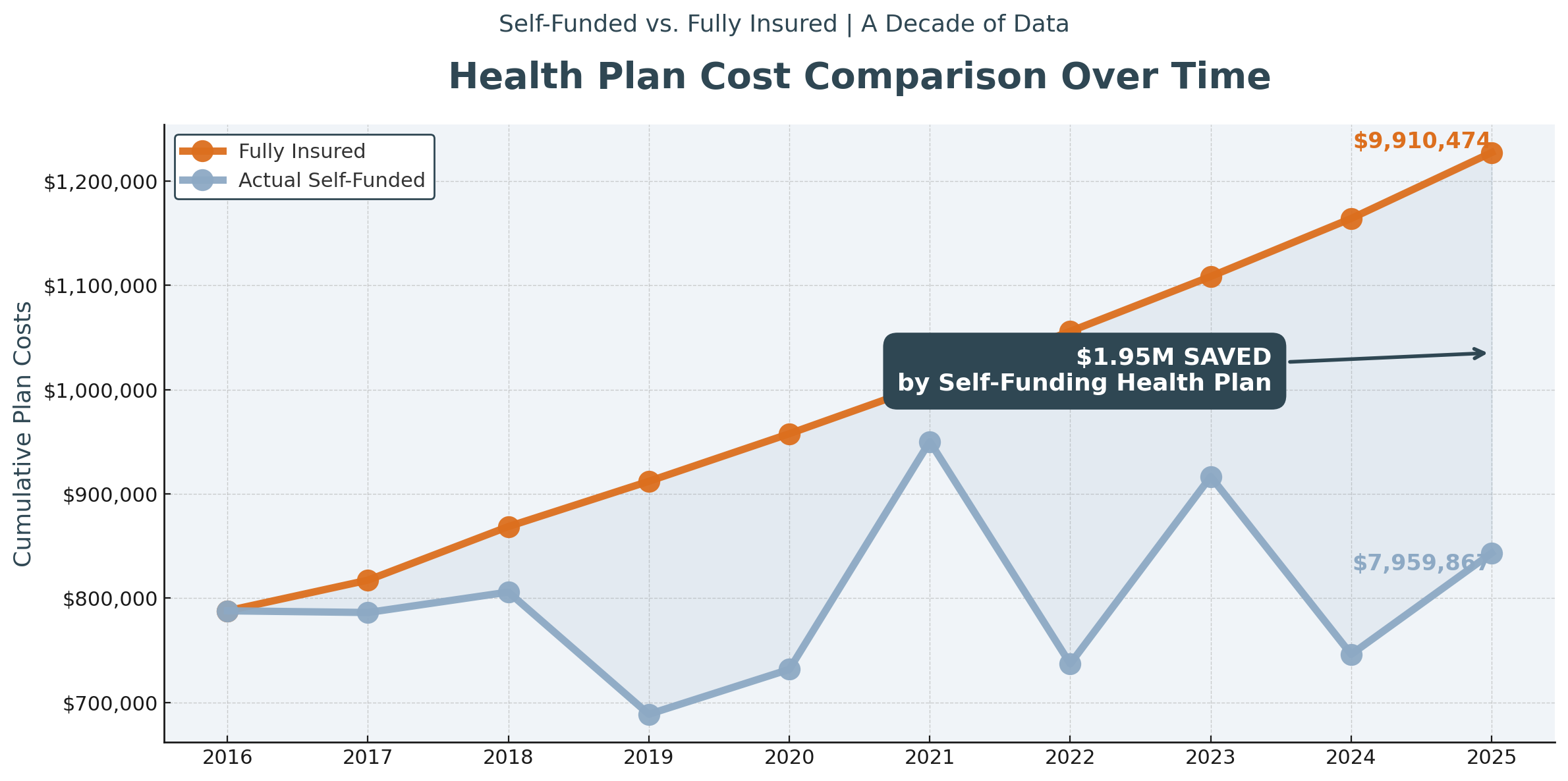

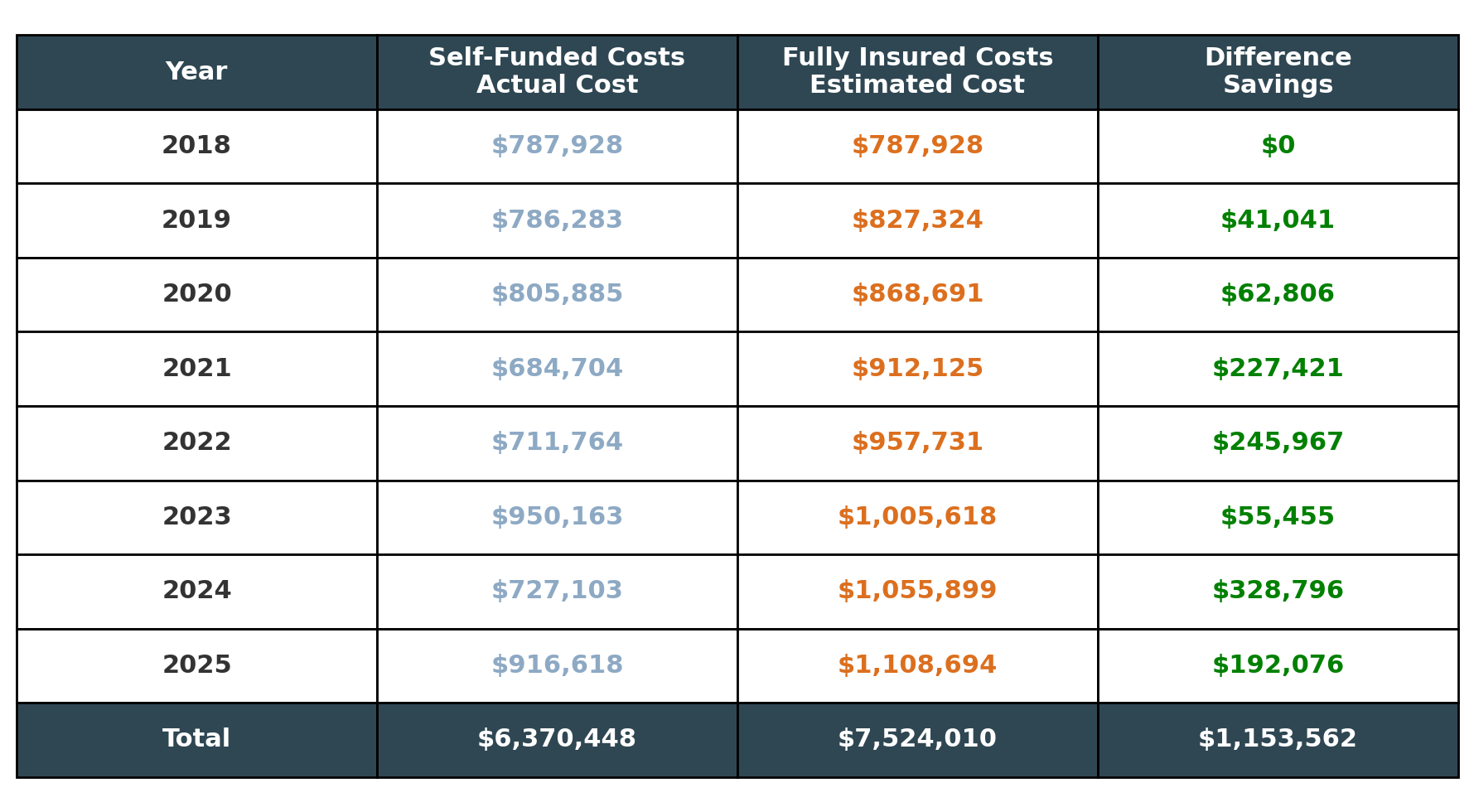

Long-Term Cost Comparison

For employers with fewer than 200 covered employees, annual premium increases have become a frustrating and often unquestioned part of doing business. If your group has a rough claims year, you can expect double-digit increases. If your group has a great year, you’re still likely to see a 5–7% hike simply because you're pooled with other groups that didn’t fare as well. This broken logic has become so routine that many employers don’t even seek competitive quotes when their renewal increase is “only” 5%.

But here’s the truth: Most groups experience three or four good years of claims for every one bad year. In a self-funded plan, you feel that cycle — costs may rise in a bad year, but they drop back down whenclaims normalize. With fully insured plans, the premiums only go one direction: UP.

The chart below shows how self-funded plans consistently out perform fully insured models over a 10-year span - not just in controlling cost spikes, but in returning savings back to your business. Over the longterm, self-funding wins financially almost every time.

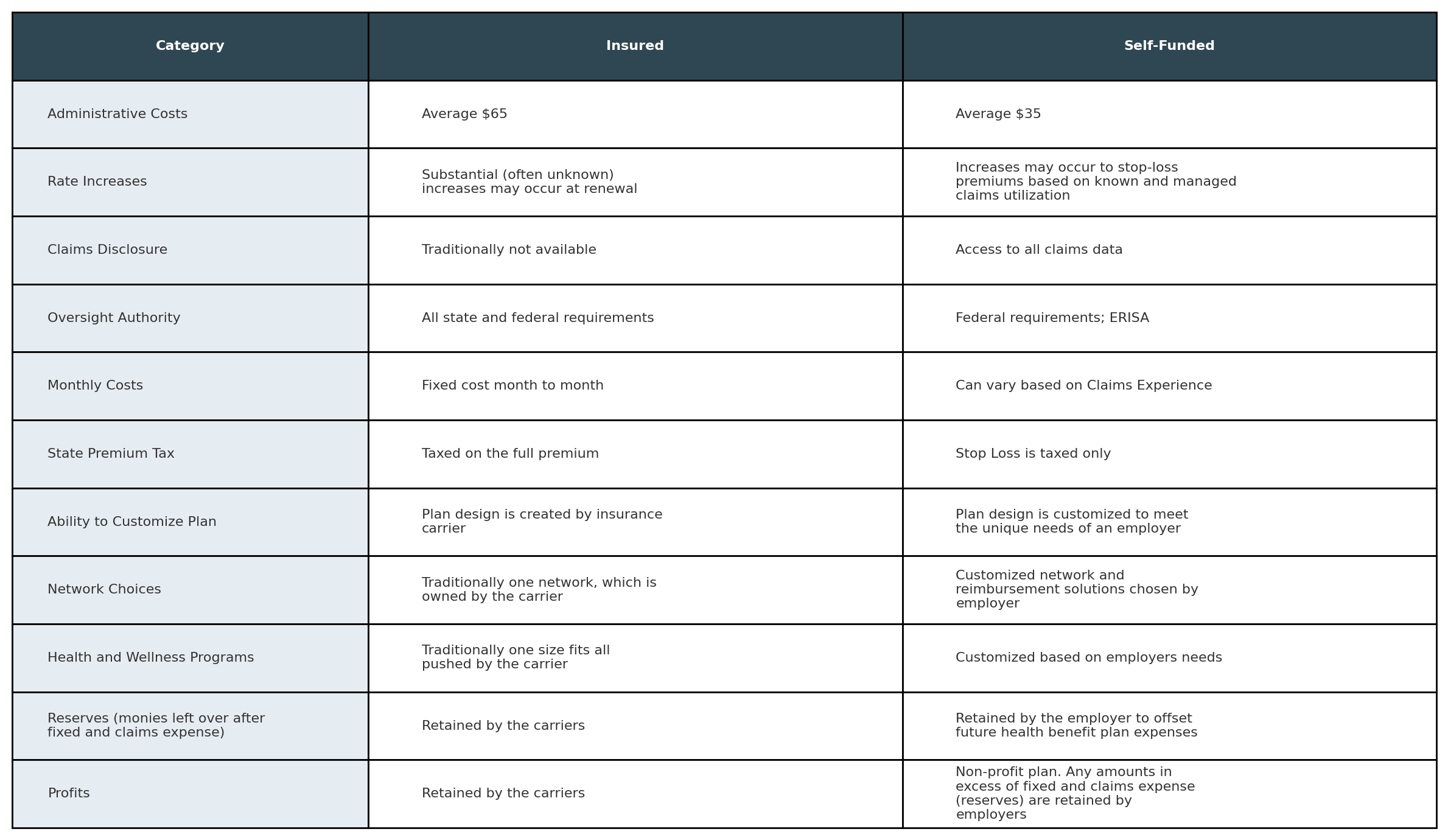

How Do They Compare?

Both Fully Insured and Self-funded benefit plan options have a place in today’s healthcare space. Some employers are not comfortable, assuming risk, and so an Insured health benefit plan is the most viable option.For employers that want to take a more active role, a customized Self-funded health plan with associated risk management/mitigation tools allows the employer to manage its own destiny.

Long-Term Cost Comparison

Request a Coverage Review Now

Are you overpaying for underperforming coverage? Let us analyze your current plan and identify hidden risks and opportunities.

Pricing

Insured healthcare premiums are known to substantially increase year to year, with little ability by the employer to have any impact on the outcome, other than reducing participant benefits or charging participants more for coverage. This lack of control is why 90% of Fortune 1000businesses choose to Self-Fund their healthcare benefits. Self-FundedAdministrative Services Only (ASO) health benefit plans administered by carriers have an associated administrative fee of $65 per employee per month(PEPM), on average. Self-funded health benefit plans administered by a professional Third-Party Administrator have an associated administrative fee of just $35 per employee per month (PEPM). Why pay more to have the health benefit plan needs of your employees dictated to you?

Plan Designs

Being forced to have the same health benefit plan offerings as everyone else is far from ideal. Businesses are unique, so why aren’t plan designs unique too? With Self-funding, flexibility and customization are key.With a trusted Third-Party Administrator (TPA) by your side, you will have confidence that you are selecting the health benefit plan that meets your company’s needs, while also keeping your employees healthy and productive.

Network

Insurer provider networks typically include 96% of all providers in the US. Does an employer really benefit by having 900,000 providers to choose from? There’s nothing ‘preferred’ in a Preferred ProviderOrganization (PPO) that includes 96% of all providers! What’s most important?We believe it is finding a network that meets the needs of your Plan’sParticipants. Some employers choose to forego the network all together and use a variety of location-specific network alternatives to achieve drastically higher levels of savings. Would you rather receive a 55% network discount on a$1,000,000 bill or a 40% discount on a $500,000 bill?

Long-Term Effects

So what role does your health benefit plan play in the grand scheme of your business? A fear of many employers thinking about Self-funding, is that a bad plan year with high claims experience could effectively mean the end of their business. Stop-loss insurance is a policy designed to limit claim exposure to a specific amount. A Self-funded employer purchases stop-loss insurance to ensure that catastrophic claims (specific policy) or numerous claims (aggregate policy) do not upset the financial reserves of theSelf-funded plan. A quality Stop-loss insurance policy is a key risk management component of any quality Self-funded program. The bottom line is that Insured health benefit plans are designed for employers that want to pay a premium and relinquish control of their health plan. For employers that want to maintain that control and design a customized health benefit plan that suits the needs of their employees and business, Self-funding is the solution. To determine the best option for you, speak with a trusted HUB Benefits Advisor or Consultant.

Get the Support You Deserve

Win more mid-market deals with Fox Everett. Our flexible solutions, human-first service, and producer-friendly tools make us the partner you need to succeed.